Home /

Home / China’s Lithium Battery Supply Chain Continues Strong Growth in May 2025

Table of Contents

The global lithium battery industry maintained strong momentum in May 2025, with China’s battery supply chain showing significant year-on-year growth across key materials and battery production segments. Recent industry data indicates that leading battery manufacturers and upstream material suppliers are continuing to expand production capacity to meet accelerating demand from electric vehicles (EVs), energy storage systems, and consumer electronics markets.

Top Battery Manufacturers Maintain Rapid Expansion

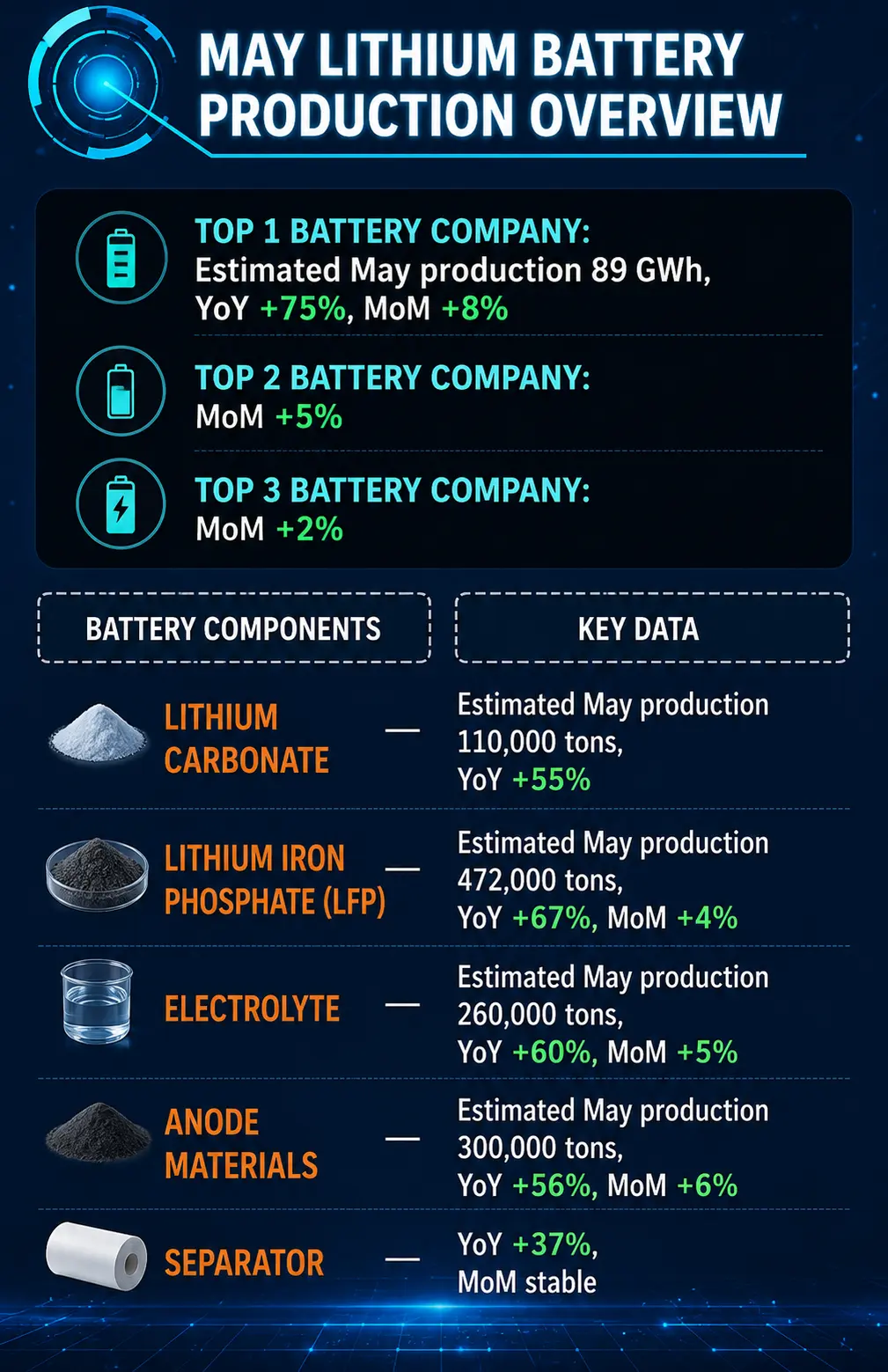

According to the latest production schedule estimates, the leading battery manufacturer is expected to reach approximately 89 GWh in May output, representing an impressive 75% year-on-year increase and an 8% month-on-month rise. Meanwhile, the second and third largest battery producers are also expected to post steady monthly growth of 5% and 2%, respectively.

This strong production performance reflects continued confidence in the EV and energy storage sectors, especially as global automakers ramp up electrification strategies and governments continue supporting renewable energy adoption.

Lithium Carbonate Supply Continues to Rise

Lithium carbonate, one of the most critical raw materials for lithium-ion batteries, is projected to reach around 110,000 tons in May production, marking a substantial 55% year-on-year increase.

The rapid increase in lithium carbonate production highlights ongoing investments in lithium refining capacity and the growing demand for battery-grade lithium materials worldwide.

LFP Battery Materials Show Exceptional Momentum

Lithium Iron Phosphate (LFP), one of the fastest-growing battery chemistries in the EV market, is expected to achieve approximately 472,000 tons in May production. This represents a remarkable 67% year-on-year growth and a 4% increase compared to the previous month.

LFP batteries continue gaining market share due to their lower cost, improved safety, and long cycle life, making them highly attractive for electric vehicles and large-scale energy storage applications.

Electrolyte and Anode Material Production Expands

Electrolyte production is forecast to reach approximately 260,000 tons, reflecting a 60% annual increase and 5% monthly growth. At the same time, anode material output is projected at around 300,000 tons, with a strong 56% year-on-year increase and 6% month-on-month growth.

These figures demonstrate that the entire battery materials ecosystem is scaling rapidly to support rising downstream battery demand.

Separator Market Remains Stable

Battery separator materials also maintained healthy growth, recording a 37% year-on-year increase, while remaining relatively stable on a monthly basis. Stable separator supply is essential for ensuring battery safety and manufacturing efficiency across the industry.

Outlook for the Global Battery Industry

The latest production data reinforces the view that the lithium battery industry remains in a strong expansion cycle. Growing adoption of electric vehicles, renewable energy storage, and AI-driven power infrastructure is expected to further accelerate demand for lithium-ion batteries over the coming years.

As battery manufacturers continue investing in capacity expansion and supply chain optimization, China remains a critical hub in the global energy transition and clean technology ecosystem.

Talk to the Manufacturer

Resources & Insights

7.4V 4400mAh Li-Polymer Battery Pack for Ski Gloves and Heated Clothing

2026-07-22

7.4V 5200mAh Rechargeable Battery Pack for Heated Jackets and Heated Clothing

2026-07-22

7.4V Rechargeable Lithium-Ion Battery Pack for Heated Gloves & Heated Apparel

2026-07-22

1000mAh USB-C rechargeable lithium-ion battery for headlights (3x AAA size)

2026-07-22